The Common Chart of Accounts (CCOA) fulfills a vital role for capturing operational, managerial, and external financial activity to meet campus and UC wide financial reporting.

It organizes this financial activity by a series of segments that, put together, are meaningful for appropriately categorizing revenue and expenses. The combination of these segments is called a chartstring. When designed thoughtfully and used consistently, the chartstrings inform us of where money comes from and where it goes, enabling reporting and analysis at all levels across campus (and the UC system, thanks to the “common” elements of the new chart.)

Take the virtual Common Chart of Accounts training!

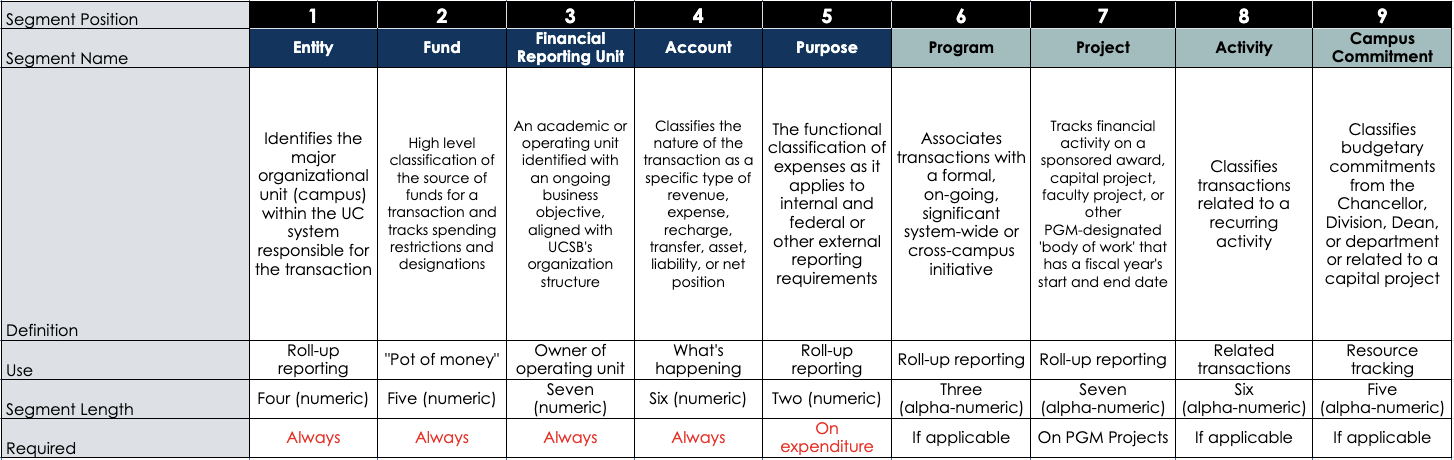

Common Chart of Account Segments

The following is a summary of the UCOP Common Chart of Accounts (CCOA) segments and descriptions. You can also view and download a PDF guide that contains this information and relevant examples.

| # | CCOA Segment | Description |

| 1 | Entity | Identifies the major organizational unit (campus) within the UC system responsible for the transaction |

| 2 | Fund | High-level classification of the source of funds for a transaction and tracks spending restrictions and designations |

| 3 | Financial Reporting Unit (FRU) | Represents an academic or operating unit identified with an ongoing business objective, aligned with the UCSB’s organization structure |

| 4 | Account | Classifies the nature of the transaction as a specific type of revenue, expense, asset, liability or fund balances; often referred to as the 'natural' account |

| 5 | Purpose | The functional classification of expenses as it applies to internal and federal or other external reporting requirements |

| 6 | Program | Associates transactions with a formal, on-going, significant system-wide or cross-campus initiative |

| 7 | Project | Tracks financial activity related to a sponsored award, a capital project, or a "body of work" that has a start and end date often spanning fiscal years. |

| 8 | Activity | Classifies transactions related to a recurring activity |

| 9 | Campus Commitment |

Classifies budgetary commitments from the Chancellor, Division, Dean, or department or related to a capital project |

CCOA Request Form

As departments are reviewing their new CCOA and wish to request a change (add, change, inactivate) a segment of their chartstring, please follow these instructions to submit a CCOA Request Form via Smartsheet. This form will initially route to either your Assistant Dean or your divisional CFO, depending on your department.

Please note:

- Any existing (legacy) accounts that have transaction data within the last two years will need to be mapped to a FRU, even if the account is not currently active.

- If departments need to make a change to several chart segments, please reach out to your divisional CFO to request a bulk change template.

- The deadline to request a change is Wednesday, April 16 in order for the data to convert to Oracle Financials Cloud (OFC) on July 1. Please check with your divisional CFO for any earlier deadlines.

- Approved segment changes will be visible in the CCOA Explorer Tool. They will not be visible in OFC for User Acceptance Testing.

For support with using the CCOA Explorer Tool and understanding how your department will use the new chart, we encourage you to attend our office hours.

Why are we changing our Chart of Accounts?

In order to improve the quality and consistency of the reporting of financial data, the University of California, Office of the President (UCOP) coordinated a collaborative project with all of its campuses and medical centers to design a Common Chart of Accounts (CCOA). UCSB will be adopting the CCOA by July 2025. Many of the UC campuses, including UC Santa Barbara, decided to adopt the CCOA while transitioning to a modern financial system with the implementation of Oracle Financials Cloud.

Benefits of the new CCOA

- Chartfields have a single use with a clear and consistent definition

- Simple, intuitive, and able to adapt to growth and change

- Captures sufficient transactional detail at the project, departmental, college, campus, and institutional levels to support financial and budgetary analysis and management

- Enables standardized, accurate, and reliable internal and external reporting at detail and summary levels by:

- Organizational entity

- Fund type

- Account structure

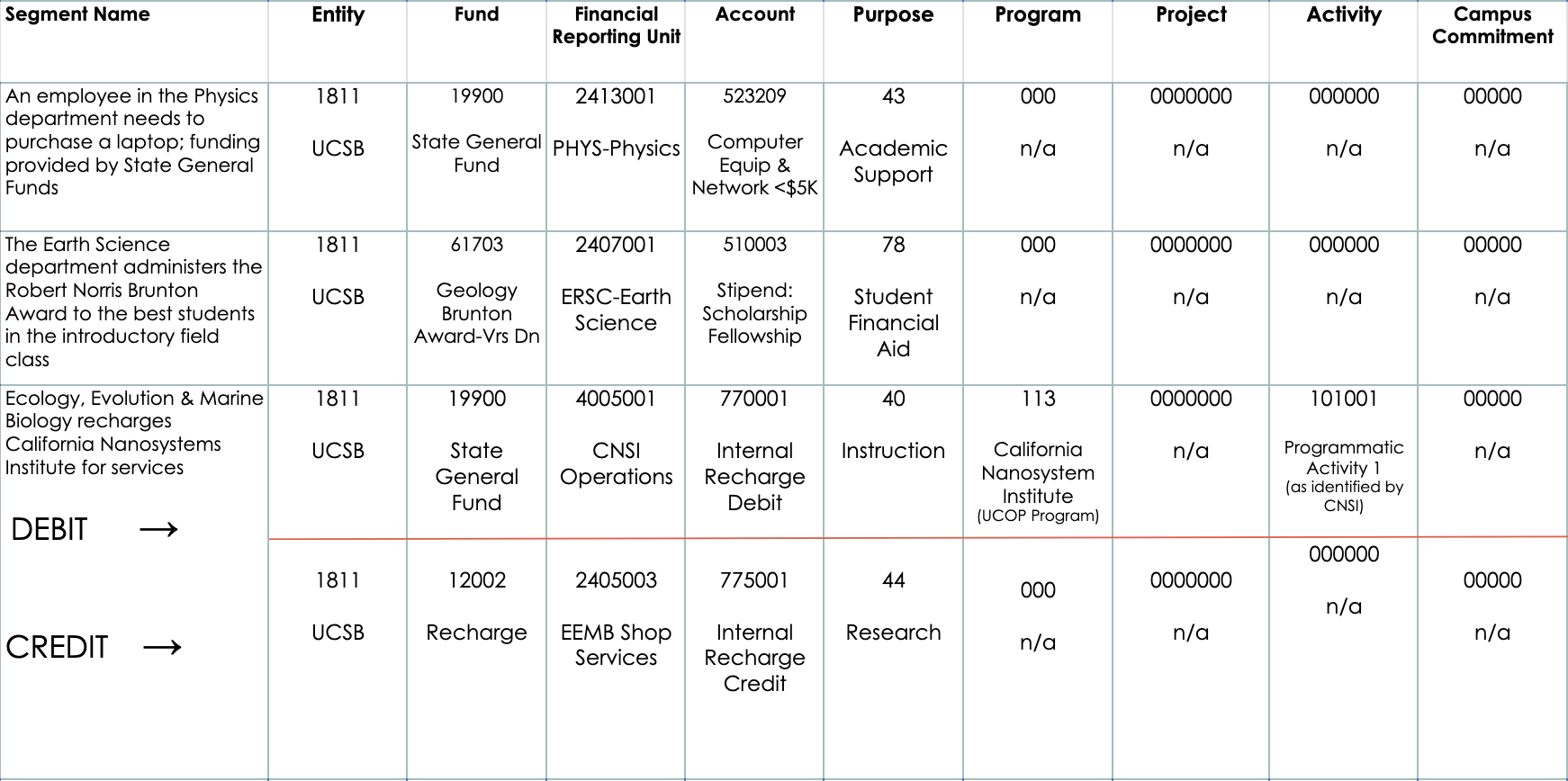

CCOA Segment Examples

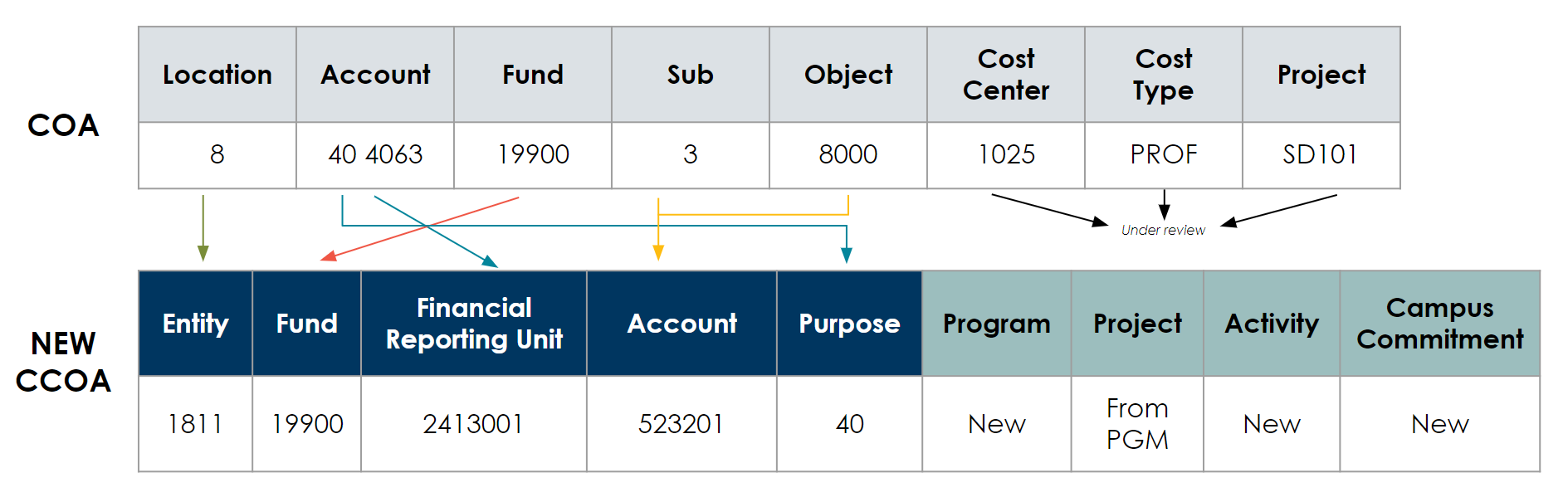

Translating the Current COA to the New CCOA

Important Changes

- For most segments, a hierarchical tree structure was created to facilitate roll-up reporting

- Fund numbers associated with sponsored projects will change

- The dept. ID remains the "home department," but a financial transaction requires a Financial Reporting Unit (FRU) value to specify “who”

- The Account number becomes the “natural classification” of an expenditure similar to the current Object Code; will specify “what;” coding for Sub-Accounts is no longer needed

- The Account numbers are not owned by a specific department; the owner of a transaction is identified by the FRU

- The purpose of an expenditure, e.g., Instruction, Research, Student Financial Aid, etc., is currently represented by the first-two digits of the Account; the Purpose is now a separate segment

- Program, Activity, and Campus Commitment values are used for tracking budgetary and transactional activity for consolidated reporting

Implementing a New CCOA

CCOA Explorer Tool in Power BI

We are excited to share that the “CCOA Explorer Tool” is available for use in Microsoft Power BI. This new application allows departments to view the new chart structure and hierarchy for their area. By utilizing this tool, departmental staff can familiarize themselves with their specific Common Chart of Accounts structure and enhance their understanding of the overall chart organization and reporting. Visit the CCOA Explorer Tool page for more information, instructions, and resources for using the application.

Completed

- Define segments, purpose and usage

- Refine how UCSB will use segment

- Determine UCSB segment name and definition

- Confirm the field length and type

- Determine sequential order

- Identify high-level hierarchy

- Map current-state segments to future-state segments

- Define chart of accounts governance

What's Next

- Determine the need to refine values and hierarchies

- Finalize mapping to begin data conversion and integrations